“A borrower ends up being a slave to whoever lends them money.” – Proverbs 22:7

Debt can at times seem like the gloomy cloud hanging over your head, snatching your peace and restricting your financial future. As one who has been in financial education for years, helping dozens of individuals and families get rid of thousands of dollars in debt, here’s what I can tell you: it’s very doable to get out of debt fast, not just possible with a plan, discipline, and the right strategies, but within months.

Alright, folks, buckle in – everything that’s usually taught to clients over a bunch of meetings drinking from the fire hose when the credit card payments, student loans and personal debt all start drowning you. From best repayment methods to real-world success stories, consider this your blueprint for getting out from under the thumb of debt.

Understand Your Debt Situation First

To obliterate debt, you must first understand your debt. Begin with a simple spreadsheet or use free apps such as Undebt.it or Tally. Here’s how to get started:

- List all your debts: Creditor, balance, interest rate, and minimum monthly payment

- Sort out what the debt is from: Credit cards, student loans, medical bills, and the notorious payday loans, car loans, etc.

Prioritise based on impact: High-interest debts (like credit cards) often cost you the most over time.

Example: I had a client, Sarah, who had five credit cards and two student loans. ‘ You’re listed all of these,’ I said. She calculated that she was spending over $600/month just on interest income. ‘You’re listing them in black and white,’ Angel said, acting as if nothing could be done without this information.

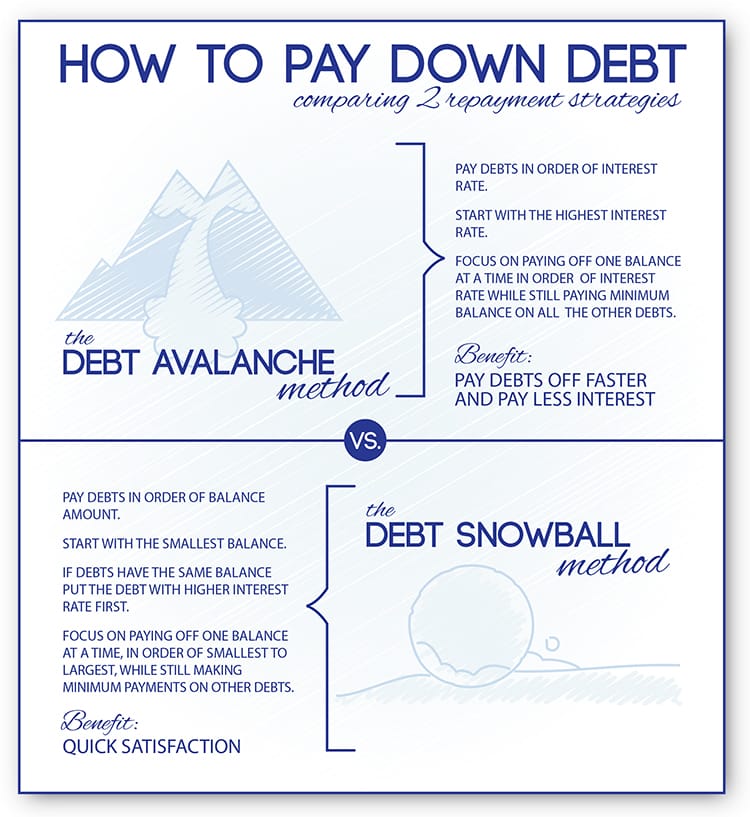

Choose a Proven Debt Payoff Method

There are two common strategies when it comes to paying off debt: the Debt Snowball and the Debt Avalanche.

Debt Snowball:

- Pay off your smallest debt first, regardless of the interest rate.

- Superb for motivation and ‘quick wins’.

- A momentum builder.

- Debt Avalanche:

Pay off the debt that bears the highest interest first. - Saves more over time.

- Disciplined; but mathematically optimal.

Now, suppose you have two debts:

Credit Card A: $3,000 at 25% APR

Credit Card B: $800 at 17% APR

Snowball Method: You’d pay off Card B first to get rid of a balance and build up some steam.

Avalanche Method: You’d direct your attention to Card A to cut down the full interest burden.

I tend to think you should go with the method that fits your personality. If you need to feel progress quickly, go with the Snowball. If you’re analytical and numbers-driven, the Avalanche is your friend.

Create a Budget That Prioritizes Debt Repayment

Without a budget, you’re driving blind. I teach my clients to adopt a Zero-Based Budget, which means every dollar has a job.

Steps to create it:

- Track your income: Know your take-home pay.

- List all expenses: Fixed, variable, and discretionary.

- Assign every dollar: Include debt payments as top priority.

- Cut ruthlessly: Drop subscriptions, limit eating out, shop with a list.

Real-World Tip: I worked with a single dad who switched from daily takeout lunches ($300/month) to home-packed meals. He redirected that money to pay down debt and saved over $3,000 a year.

Increase Your Income to Accelerate Payments

When cutting isn’t enough, it’s time to earn more.

Quick Ideas to Increase Income:

- Freelance: Sites like Upwork or Fiverr for writers, designers, or marketers.

- Sell items: Use Facebook Marketplace or eBay.

- Part-time job: Weekend or evening work at a local store or gig economy (Uber, DoorDash).

- Monetize skills: Tutoring, music lessons, web design.

Example: A couple I coached started flipping furniture on weekends. Within three months, they made $2,400 extra and paid off their car loan.

Use Debt Consolidation Wisely (If Applicable)

Debt consolidation is the double-edged sword. Use it wisely and it simplifies your payments and lowers your interest. Use it poorly and it leads to more spending.

Balance Transfer Cards: Take the 0% APR and pay it off before the promo’s over and this helps pay down debt faster.

Personal Loans: Fixed-rate loans from $2,000 to $35,000 for debt consolidation of high-interest debts.

Credit Counseling: Negotiates reduced rates for clients with credit card companies, conducted by a nonprofit agency.

Watch out for services asking for money before they’ve done anything or claiming they’ll do miraculous things. Take a good look at the details

Avoid Common Debt Payoff Pitfalls

The road to debt freedom is littered with temptations. Be warned:

- Don’t close all accounts at once. It could tank your credit score.

- Keep an emergency fund. Even if that teeters you at the brink of debt, don’t.

- Stay away from payday loans and all those quick-fix scams; they are traps.

- Stay emotionally balanced: Shame, guilt, or impulsivity will derail your progress.

Hint: Join a support group or online community like Reddit’s r/personalfinance to stay in line.

Tools, Apps, and Resources That Help

Budgeting:

- YNAB (You Need A Budget): Best for zero-based budgeting

- Mint: Great free tool for tracking

- EveryDollar: Simple, intuitive interface

Debt Tracking:

- Undebt.it: Free tool to visualize debt payoff methods

- Tally: Helps manage credit card payments efficiently

Books:

I Will Teach You to Be Rich by Ramit Sethi

The Total Money Makeover by Dave Ramsey

Your Money or Your Life by Vicki Robin

Real-Life Success Story

Jenny’s Path to Money Independence

Two years ago, single mom Jenny Parker would soon have hit a financial crisis. She had her child in one hand, 10 pounds in the other, and debt amounting to 7,000 pounds. Today she has emerged from this crisis and is on to a home deposit. The snowball method’ andcadence cash’ kept her interest bogged with the lowest balance first but weekly loan repayments and that being only on the smallest balance made it that much more supportable while heeding the snowball modes and then killed off the debt. At times she would rent out garden tools or yard sale various items on eBay which helped her push up the income less directly but by cost-effectively maintaining a ‘no-debt’ lifestyle; in real time also saving towards having a house of her own.

Source: The Sun

Conclusion: Your Debt-Free Future Starts Now

Becoming debt-free fast isn’t just a goal—it’s a transformation. The process will challenge you, yes, but it will also empower you. I’ve seen clients go from paycheck-to-paycheck to saving for a home within 18 months. I’ve witnessed people erase $20,000 in debt in under a year.

The formula is simple: Know your numbers. Choose your method. Cut ruthlessly. Earn more. Stay the course.

You’ve got this.

Need a starting point? Download my Free Debt Snowball & Avalanche Tracker and take the first step toward the financial freedom you deserve.